Flex is helping women’s health brands access a $150 Billion pre-tax market — here’s how

One of the smartest untapped levers in women's health

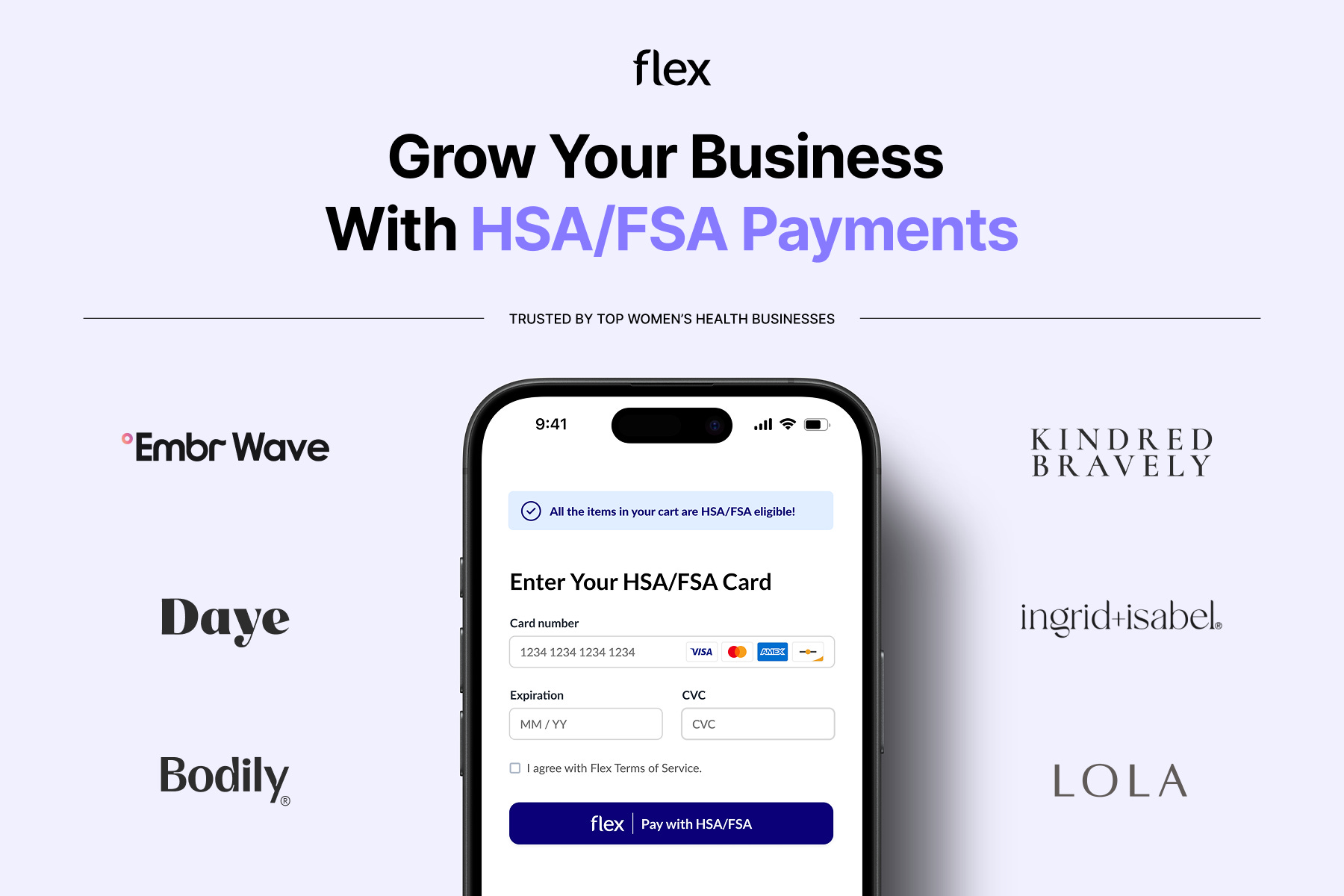

Startups like Kindred Bravely, Daye and Embr Wave are already using Flex to unlock hidden healthcare dollars. Now, the fintech wants more women’s health brands to know how to follow their lead.

Every women’s health founder knows the challenge: you’ve built something genuinely useful — maybe even essential — but your customers are hesitating at checkout.

Whether it’s a pelvic floor trainer, a hot flash wearable, or a subscription-based therapy app, price sensitivity still stalls the sale. And with most of these purchases sitting outside traditional insurance coverage, the friction point is real.

But what if the customer wasn’t actually paying full price?

If she uses her Health Savings Account (HSA) or Flexible Spending Account (FSA) dollars, she’s spending money that’s already been deducted from her paycheck — tax-free. The brand still receives the full price, but the customer’s effective cost drops by 20–30%. No discounts. No margins sacrificed.

It’s one of the smartest untapped levers in women’s health. And yet, many founders still assume it’s not available to them or too complicated to implement.

“Most founders know HSA/FSA dollars are out there, but are confused as to how to access them. HSA/FSA ends up at the bottom of the list because it's perceived as being too-complicated,” says Sam O’Keefe, co-founder of Flex.

“We simplify the process to accept HSA/FSA payments and open up a whole new revenue stream for our partners."

The hidden budget most founders overlook

In the U.S., an estimated $150 billion is set aside in HSAs and FSAs — that’s pre-tax income that consumers can use to pay for qualified health expenses. These accounts are funded by employees (and sometimes employers) and are meant to cover costs that insurance doesn’t.

“It’s not just about figuring out what qualifies for HSA or FSA funds—it’s about making those funds easy for consumers to spend,” O’Keefe says.

Under IRS rules, a retailer that wants to accept HSA/FSA cards must prove that each item is a qualified medical expense and split the cart at checkout to keep eligible and ineligible items separate before the purchase can be completed. Building that kind of infrastructure in-house doesn’t make sense—just as brands don’t create their own buy-now-pay-later systems—and most existing e-commerce payment providers don’t support it.

That’s where Flex comes in. Flex lets DTC businesses accept HSA/FSA payments without hassle, handling every regulatory requirement so merchants and shoppers don’t have to think about compliance. Its streamlined checkout lets consumers pay with their benefits cards in seconds, boosting revenue for the brand.

“Imagine telling customers, ‘Yes, your pelvic-health device is HSA/FSA-eligible—use your benefits card today.’ That changes the game,” O’Keefe adds.

A changing definition of healthcare

“There’s this mental image we all have of HSA/FSA being just for prescriptions or crutches,” says O’Keefe.

“But that’s outdated. The rules are evolving — especially since 2020, when the CARES Act finally made menstrual products eligible. It was a step, but a long-overdue one.”

That moment — when tampons, pads, and period products were officially recognised as healthcare expenses — was a milestone. It signalled what many in femtech have argued for years: women’s health is health.

Now Flex already works with a growing list of women’s health startups, including:

Kindred Bravely, makers of postpartum and nursing wear

Milkify, a breast milk freezing service

Daye, the gynaecological health platform

Embr Wave, a wearable for hot flashes and temperature regulation

“We’ve seen huge traction in women’s health, from menstruation to fertility, to birth and postpartum and menopause,” says O’Keefe.

“Products that support real, lived health needs — but that have been overlooked by traditional definitions of ‘medical.’”

Flex also operates a curated marketplace to help consumers discover what qualifies — and avoid letting their HSA/FSA funds expire.

Expanding accessibility - with big benefits for brands

The shift is still far from complete. Many everyday women’s health needs remain outside the boundaries of what HSA/FSA will cover.

Flex is currently supporting a petition to expand eligibility across a broader range of women’s health essentials - the kinds that seem obvious to anyone who’s been pregnant, gone through menopause, or struggled with fertility.

Among the list: nursing bras, postpartum meals, lactation massagers, sexual wellness tools, and essential postnatal nutrition like iron and omega-3 supplements.

In the meantime, Flex makes it easier for customers to access these products by issuing LMNs (letters of medical necessity) where needed — a workaround that opens up HSA/FSA without a trip to the GP.

From a business perspective, the upside is hard to ignore. Flex’s own data shows that 67% of customers said they wouldn’t have purchased without the HSA/FSA option, and brands that enable it see, on average, a 30% boost in conversion.

“Accepting HSA/FSA makes your product more affordable, attracts new customers, and increases cart sizes,” says O’Keefe.

And for international brands trying to navigate the U.S. system?

“We work with a number of international businesses who want to grow their US revenue,” she says. “HSA/FSA can be a great growth lever for them too.”

Flex is working on both fronts: helping brands accept pre-tax payments where eligibility already exists, and campaigning to expand what’s covered.

“It’s a win-win,” says Sam.

“Customers get access to products they didn’t realise they could afford. And brands get discovered by people actively looking to spend.”

Founders: what you can do

If you’re building a women’s health product, you might not need to change a thing — just how you support your customers in paying for it.

Head to Flex to see if your product qualifies - many already do - and find out how to enable HSA/FSA payments with Flex’s free consultation.

To get started with Flex: https://www.withflex.com/contact