What counts as women’s health? Rethinking how we measure investment in women’s health

FutureFemHealth is introducing a new framework for analysing investment across women’s health.

Starting with our Q2 2026 Funding Tracker (out in early July), FutureFemHealth is introducing a new framework for analysing investment across women’s health.

Rather than asking whether a company ‘is’ or ‘isn’t’ a women’s health company, we ask two questions:

What type of health need is being addressed?

How exposed is the company to women’s health?

Together, these two lenses provide a more nuanced view of where capital is flowing, from pure-play women’s health companies through to broader healthcare businesses making meaningful investments in women’s health.

The goal is to provide a more transparent and consistent way of understanding an increasingly complex market.

Why we built it

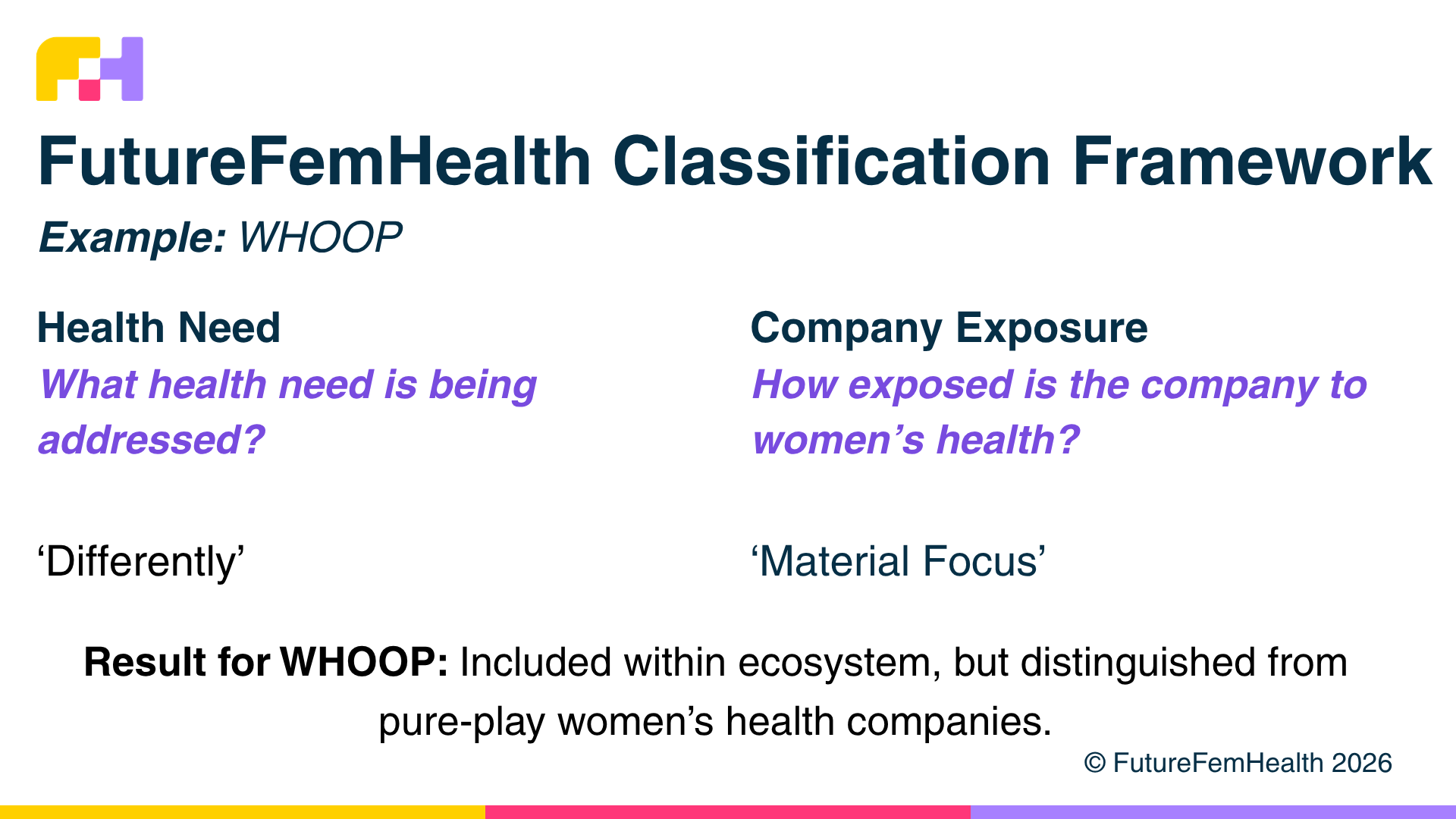

The challenge became obvious as companies such as WHOOP, Oura, UroMems (incontinence) and Hemi Health (migraine) began raising funding.

Should these count as women’s health investments?

The answer felt like yes - but not in the same way.

WHOOP is a good example. The company has invested heavily in female physiology research, menstrual cycle insights and women’s health features. Ignoring that would overlook an important shift.

Yet, counting its entire $575 million funding round as women’s health investment would also distort the market. The raise was almost as large as every other women’s health funding round in Q1 2026 combined!

The same tension exists across healthcare. Some companies address conditions that disproportionately affect women. Others are redesigning products around biological sex differences. Some have made women’s health a major commercial priority despite operating across much broader markets.

Traditional funding trackers struggle to capture these distinctions.

As a result, we risk both overstating and understating the market. We inflate women’s health funding by including companies only partially exposed to the category, while simultaneously overlooking businesses where women’s health is hiding in plain sight.

The questions we wanted to answer were simple:

How much capital is flowing into pure-play women’s health companies? (most existing trackers do this part well)

How much is flowing into businesses where women’s health is a major commercial focus?

How much is flowing into broader healthcare companies investing in women’s health as part of a wider strategy?

Answering those questions requires two separate lenses.

An overview of the FFH Classification Framework

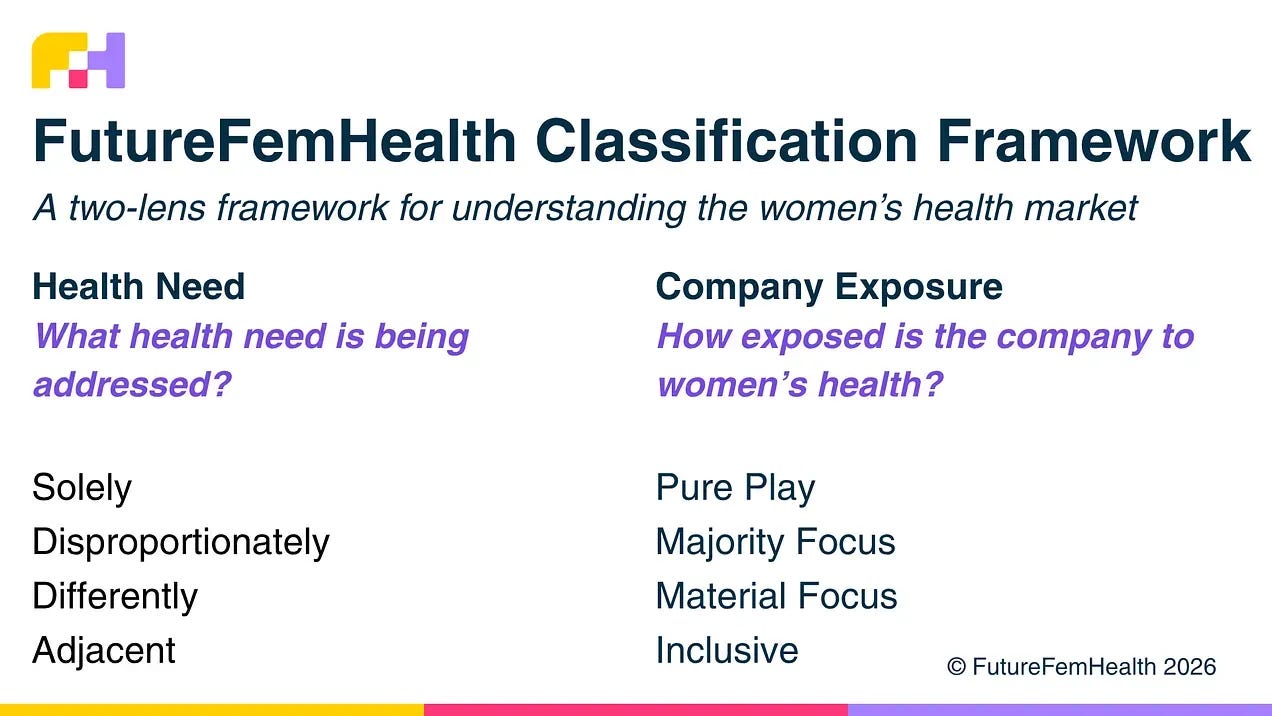

Lens #1: What health need is being addressed?

The first lens classifies the underlying health need and uses a well-established framework:

Solely: Conditions that only affect women, such as menstruation, pregnancy, menopause and endometriosis.

Disproportionately: Conditions affecting everyone but where women experience a greater burden of disease, including osteoporosis, urinary incontinence, migraine, autoimmune disease and Alzheimer’s disease.

Differently: Conditions where biological sex influences symptoms, diagnosis or treatment, such as cardiovascular disease, obesity, metabolic health, sleep and mental health.

Adjacent: Areas commercially relevant to women but where women’s health is not the primary lens, including consumer wellness, longevity, male contraception, and healthcare infrastructure.

Lens #2: How exposed is the company to women’s health?

The second lens looks at the business itself.

In simple terms:

If women’s health disappeared tomorrow, how much of the business would remain?

We classify companies into four categories:

Pure Play: Women’s health is the business.

Majority Focus: Women’s health represents most, but not all, of the company’s activity.

Material Focus: Women’s health is an important strategic focus alongside broader products or markets.

Inclusive: The company serves women, but women’s health is not a material driver of the business or investment case. (In this case, the company is unlikely to be included).

Why use two lenses?

A single label doesn’t tell us the whole story. Migraine, for example, disproportionately affects women, but companies addressing migraine vary enormously in how central women’s health is to their strategy.

The same is true for wearables. A company may invest heavily in female physiology research and cycle tracking while generating most of its revenue from broader health and fitness markets.

Looking only at the health need - or only at the company - misses part of the picture.

Together, the two lenses capture both.

Finally, an important feature of the framework is that it helps us explain both what we include and what we don’t. Not every company with a predominantly female customer base is a women’s health company, just as not every business addressing women’s health will identify itself as one. By assessing both the health need and the company’s strategic focus, we can make those decisions more consistently and transparently.

What does this look like in practice?

Let’s return to WHOOP.

Under a traditional funding tracker, WHOOP either counts as a women’s health company or it doesn’t. But, neither answer feels particularly satisfying.

Excluding the company ignores its growing investment in women’s health. Including all of its funding overstates the amount of capital flowing into dedicated women’s health businesses.

Our framework allows us to recognise both the health need being addressed and the company’s overall exposure to women’s health.

The same principle can be applied to companies such as Oura, Hemi Health, Salvo Health, Eight Sleep and many others. Rather than forcing a binary decision, we can better reflect the complexity of today’s women’s health ecosystem.

Why this matters

Women’s health is expanding well beyond fertility, pregnancy and menopause into mainstream healthcare.

As that happens, understanding where capital is flowing becomes both more important and more complicated.

We do not claim this framework is the definitive answer. The category is evolving quickly, and reasonable people will disagree on individual classifications.

Our aim is simply to provide a more transparent and consistent way of understanding the market.

Because before we can decide whether women’s health is underfunded, we first need to agree on what we’re counting.

See the framework in action

The FutureFemHealth Classification Framework will now underpin our funding trackers, M&A analysis and broader market intelligence.

FutureFemHealth Pro subscribers receive quarterly funding trackers, M&A trackers and deep-dive analysis applying the framework across every tracked deal.

If you’d like to understand where capital is flowing across women’s health - and why - explore FutureFemHealth Pro.

A final note: Throughout this framework we use the terms “women” and “women’s health” because they remain the most widely used terms across healthcare, research and investment. We recognise that not everyone affected by these health needs identifies as a woman, and that sex and gender are distinct concepts. Our use of these terms should not be interpreted as a statement about identity.